Looking for a way to gauge the financial health of your investment or assess a borrower’s ability to handle loan repayments? A DSCR (Debt Service Coverage Ratio) calculator does just that. It assesses the financial health of a property by comparing its Net Operating Income (NOI)—the income after operating expenses—to its total debt service, including principal, interest, taxes, and insurance. Understanding the DSCR ratio can reveal much about the safety of an investment and the borrower’s cash flow buffer.

What is a DSCR Calculator?

A DSCR (Debt Service Coverage Ratio) calculator is a fundamental tool used to determine a borrower’s capacity to handle loan repayments. It’s particularly important in commercial real estate, where lenders use it to evaluate the risk associated with a potential investment. The calculator works by analyzing the relationship between a property’s Net Operating Income (NOI) – the income generated after operating expenses – and its total debt service (which includes principal, interest, taxes, and insurance).

The resulting DSCR ratio offers a clear picture of financial health. A higher ratio means the property’s income significantly exceeds its debt obligations, making it a safer bet for the lender. It shows the borrower has a comfortable cash flow buffer to make payments reliably. On the other hand, a low DSCR could indicate potential difficulties in repaying the loan, as the income generated might not sufficiently cover the debt burden.

The Key Components of a DSCR Calculator

A DSCR Calculator uses information like net operating income and total debt service to compute the ratio. Let’s break down these components a little further:

Net Operating Income

Net Operating Income (NOI) is the income generated by a property after deducting all necessary operating expenses. It does not include capital expenditures, debt service, or depreciation.

NOI = Gross Operating Income – Operating Expenses

Let’s say a rental property generates $100,000 in annual rental income. The operating expenses, including property taxes, insurance, utilities, and maintenance, amount to $40,000. The NOI would be: $100,000 – $40,000 = $60,000

Debt-Service Amounts

This refers to the total amount of debt payments required for a specific period, usually annually. The key components of the total debt service (TDS) calculation are interest, principal, and lease payments. Interest is the cost of borrowing money, typically expressed as a percentage of the loan amount.

Principal is the original sum borrowed, which must be repaid over the loan term. Lease payments are payments made for the right to use an asset, such as equipment or real estate, for a specified period.

TDS = Principal Repayment + Interest Payments + Lease Payments

Suppose an investor purchases a rental property with a mortgage. The details of the mortgage and the property are as follows:

- Mortgage Loan Amount: $500,000

- Annual Interest Rate: 4%

- Loan Term: 30 years

- Monthly Principal and Interest Payment: $2,387

- Annual Property Lease: $12,000

To calculate the total debt service, we need to determine the annual principal repayment, interest payments, and lease payments.

| Steps | Description | Calculation |

|---|---|---|

| 1 | Calculate the annual principal and interest payment. | Annual Principal and Interest Payment = Monthly Payment × 12 Annual Principal and Interest Payment = $2,387 × 12 = $28,644 |

| 2 | Calculate the annual interest payment. | Annual Interest Payment = Loan Amount × Annual Interest Rate Annual Interest Payment = $500,000 × 0.04 = $20,000 |

| 3 | Calculate the annual principal repayment by subtracting the annual interest payment from the annual principal and interest payment. | Annual Principal Repayment = Annual Principal and Interest Payment – Annual Interest Payment Annual Principal Repayment = $28,644 – $20,000 = $8,644 |

| 4 | Add the annual principal repayment, interest payment, and lease payment to get the total debt service. | TDS = Annual Principal Repayment + Annual Interest Payment + Annual Lease Payment TDS = $8,644 + $20,000 + $12,000 = $40,644 |

How is to Calculate DSCR?

The DSCR is calculated by dividing the Net Operating Income (NOI) by the Total Debt Service. The formula looks like this:

DSCR = Net Operating Income (NOI) / Total Debt Service

This calculation gives lenders or investors an understanding of the ability of a business or property to cover its debt obligations from its operating income, helping assess its financial stability and risk level.

DSCR Calculator

Interpreting DSCR Results

Interpreting the Debt Service Coverage Ratio (DSCR) is crucial for lenders, investors, and property owners to assess the financial health and risk associated with a property. Here’s how to interpret DSCR results:

DSCR > 1

A DSCR greater than 1 indicates that the property generates sufficient net operating income to cover its debt service obligations. The higher the DSCR, the more cushion the property has to handle potential income disruptions or unexpected expenses. For example:

- DSCR of 1.25 means the property generates 25% more income than needed to cover debt service.

- DSCR of 1.5 means the property generates 50% more income than needed to cover debt service.

DSCR = 1

A DSCR equal to 1 means that the property’s net operating income is exactly enough to cover its debt service obligations. There is no additional cushion, and any minor disruption in income or unexpected expenses could lead to difficulty in making debt payments.

DSCR < 1

A DSCR less than 1 indicates that the property’s net operating income is insufficient to cover its debt service obligations. This suggests that the property owner may need to use other sources of funds to make debt payments or risk defaulting on the loan. For example:

- DSCR of 0.95 means the property generates only 95% of the income needed to cover debt service.

- DSCR of 0.8 means the property generates only 80% of the income needed to cover debt service.

Lenders and investors typically prefer properties with higher DSCRs (e.g., 1.25 or above) to ensure a sufficient cushion and lower risk of default. The minimum acceptable DSCR may vary depending on the lender, type of property, and market conditions.

It’s important to note that DSCR is just one of many factors to consider when evaluating a property’s financial performance. Other factors include the loan-to-value ratio (LTV), capitalization rate (cap rate), occupancy rates, and market trends.

How to Calculate DSCR for Vacant Rental Property?

Calculating the Debt Service Coverage Ratio (DSCR) for a vacant rental property essentially follows the same principles as calculating DSCR for an occupied rental property.

To accurately calculate the NOI, which is crucial for determining the DSCR, you need to subtract all necessary operating expenses from the property’s income. For a vacant rental property, the potential rental income would be theoretical, based on market rent estimates for similar properties in the area.

Operating expenses typically include property management fees, repairs and maintenance, property taxes, insurance, and any homeowner association (HOA) fees, if applicable. It’s important to note that capital expenditures, depreciation, and mortgage payments are not included in the operating expenses when calculating NOI.

For vacant properties, accurately forecasting the potential rental income and operating expenses is key. You might consult local market data or a property management company to get realistic figures for these estimates. The goal is to show that, even without current tenants, the property can generate enough income to cover its debts, which is crucial for securing financing or assessing the investment’s viability.

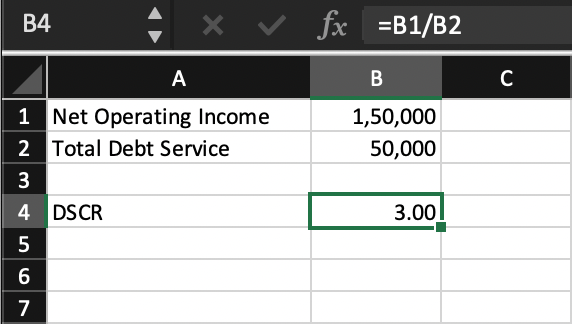

How to Calculate the DSCR in Excel?

To calculate the Debt Service Coverage Ratio (DSCR) in Microsoft Excel, you can use the following steps:

Set up your data:

- In cell A1, enter “Net Operating Income”

- In cell A2, enter “Total Debt Service”

- In cells B1 and B2, enter the corresponding values for Net Operating Income and Total Debt Service

Calculate the DSCR:

- In cell A4, enter “DSCR”

- In cell B4, enter the formula: = B1/B2

Format the result:

- Select cell B4

- Click on the “Home” tab in the Excel ribbon

- In the “Number” group, select “Number” from the dropdown menu

- Choose the desired number of decimal places (usually 2)

Here’s an example of what your Excel sheet might look like:

In this example, the DSCR is calculated by dividing the Net Operating Income (150,000) by the Total Debt Service (50,000), resulting in a DSCR of 3.00.

How to Calculate the DSCR Considering Taxes?

When calculating the DSCR, it’s also important to consider the impact of taxes on the property’s cash flow. Interest payments on debt are often tax-deductible, which means that they reduce the property’s taxable income and, consequently, the amount of taxes owed. Principal repayments, on the other hand, are not tax-deductible.

To account for this difference in tax treatment, the DSCR calculation can be adjusted to consider the tax rate.

- Determine the Net Operating Income (NOI): The NOI is the property’s income after operating expenses have been deducted. It represents the cash flow available to service debt and provide a return to the property owner. The formula is: NOI = Gross Income – Operating Expenses.

- Calculate the Annual Debt Service (ADS): The ADS is the total amount of debt payments (principal and interest) that the property must make each year. The formula is: ADS = Principal Repayments + Interest Payments.

- Adjust the interest payments for tax deductibility: Since interest payments are tax-deductible, they effectively cost less than their nominal amount. To account for this, multiply the interest payments by (1 – Tax Rate). This gives you the tax-adjusted interest payments. The formula is: Tax-Adjusted Interest Payments = Interest Payments * (1 – Tax Rate).

- Calculate the Tax-Adjusted Annual Debt Service (TAADS): The TAADS is the sum of the principal repayments and the tax-adjusted interest payments. It represents the true cost of servicing the debt, considering the tax deductibility of interest. The formula is: TAADS = Principal Repayments + Tax-Adjusted Interest Payments.

- Calculate the DSCR: Finally, divide the NOI by the TAADS to obtain the DSCR. The formula is: DSCR = NOI / TAADS.

Common Mistakes When Calculating DSCR

Here are some common mistakes to avoid when calculating the debt service coverage ratio (DSCR):

- Not Accounting for Existing Business Debt: It’s essential to include all existing business debts, such as loans, lines of credit, credit card balances, leases, and invoice financing in the total debt service calculation.

- Inaccurate Debt Amounts: Ensuring accuracy in the total outstanding principal and interest obligations is vital. Verification with bank loan officers or thorough review by an accountant or bookkeeper is recommended.

- Choice Between EBIT or EBITDA: While EBIT (Earnings Before Interest and Taxes) and EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) can both be used for DSCR calculation, EBITDA is often preferred for its simplicity. Consultation with a financial professional or lender is advised to make the best choice.

- Using Net Income Instead of Net Operating Income (NOI): DSCR should be calculated using NOI, which is revenue minus operating expenses, not including interest, taxes, depreciation, and amortization. Using net income instead can understate the DSCR.

- Not Including All Debt Service Payments: It’s crucial to include principal and interest payments on all outstanding debt in the DSCR calculation, including any balloon payments due within the measurement period.

- Miscalculating NOI: Ensure an accurate calculation of NOI by properly reviewing operating expenses and excluding one-time or non-recurring income and expenses.

- Using Outdated Financial Statements: Utilize the most recent annual financial statements, or interim statements if it’s been several months since the fiscal year-end. Relying on outdated financial information can lead to inaccuracies.

- Not Adjusting for Partial Years: When calculating DSCR for a period shorter than 12 months, annualize the NOI and debt service figures for a consistent comparison.

- Failing to Consider Off-balance Sheet Obligations: Include any equipment leases, rent payments, or other financing obligations not reflected as debt on the balance sheet but which represent committed cash outflows.

- Neglecting to Apply It Over Multiple Periods: Analyzing DSCR trends over time provides a fuller picture of financial health, revealing potential emerging problems that a single period snapshot may miss.

Pros and Cons of a DSCR Calculator

Using a DSCR calculator can significantly streamline your financial analysis process and save you time. However, it’s essential to remember that while it’s a useful tool, it should not be the only device used in your financial analysis toolbox. Always ensure you provide accurate inputs for precise results and complement its use with other financial analysis methods for a comprehensive understanding of your investment’s or business’s financial health.

| Pros | Cons |

|---|---|

| Simplified Calculations: A DSCR calculator significantly simplifies the process of determining the DSCR. Instead of manually inputting and calculating components like net operating income and total debt service, you can easily plug in numbers into the calculator for a quick result. | Limited Flexibility: While a DSCR calculator is designed for simplicity and ease-of-use, it may not accommodate complex scenarios or unique situations that could affect the DSCR calculation. |

| Time Efficiency: By streamlining the calculation process, a DSCR calculator saves investors and businesses valuable time that could be spent on other essential tasks. | Dependence on Accurate Inputs: The accuracy of the DSCR result heavily depends on the accuracy of the inputs. If you input incorrect figures for net operating income or total debt service, the resulting DSCR will be misleading. |

| Accessibility: Most DSCR calculators are readily available online at no cost, making them accessible to anyone needing to calculate the ratio. | Lack of Comprehensive Financial Analysis: While the DSCR is an important metric, it does not provide a complete picture of an entity’s financial health. Relying solely on a DSCR calculator may overlook other crucial financial considerations. |

| Variation in Formulas: Different lenders might use slightly different variations on the DSCR calculation. Ensure the calculator you use aligns with your potential lender’s formula. | |

| Limited scope: The DSCR is just one of many financial ratios that lenders and investors consider. Relying too heavily on this single metric may not provide a comprehensive picture of a borrower’s financial health. |

To know more about DSCR loans, read these guides

- Complete Guide to DSCR Loans

- What Are the Requirements for a DSCR Loan

- Pros and Cons of DSCR Loans

- Current DSCR Loan Rates

- Do You Need a Down Payment to Get a DSCR Loan

FAQs About DSCR Calculator

1. What is a DSCR calculator, and how does it work?

A DSCR calculator is an online tool that helps determine a company’s Debt Service Coverage Ratio (DSCR). To use the calculator, you’ll need to input the company’s annual net operating income and total annual debt service. The calculator then divides the net operating income by the annual debt service to provide the DSCR.

2. What is the formula for calculating DSCR?

The DSCR formula is: DSCR = Annual Net Operating Income / Total Annual Debt Service. Net operating income is calculated by subtracting operating expenses from gross income, excluding taxes and interest payments. Annual debt service includes all principal and interest payments due within a year.

3. What is a good DSCR?

Lenders typically require a minimum DSCR, which can range from 1.2 to 1.5, depending on the industry and the lender’s risk tolerance. A DSCR above 1 indicates that the company has sufficient income to cover its debt payments, while a ratio below 1 suggests potential difficulty in meeting debt obligations.

4. Can a DSCR be too high?

While a high DSCR is generally considered a positive sign, an extremely high ratio may indicate that the company is not effectively utilizing its resources to grow the business. It could also suggest that the company is not taking advantage of potential investment opportunities that could generate additional income.

5. What factors can affect a company’s DSCR?

Several factors can impact a company’s DSCR, including changes in revenue, operating expenses, interest rates, and debt structure. Economic conditions, industry trends, and competition can also influence a company’s ability to generate income and service its debt.

6. How often should a company calculate its DSCR?

Companies should calculate their DSCR regularly, typically on a quarterly or annual basis, to monitor their financial health and ability to meet debt obligations. Lenders may also require periodic DSCR calculations as part of loan agreements.

7. What should a company do if its DSCR is low?

If a company’s DSCR is low, it should take steps to improve its financial situation. This may include increasing revenue, reducing operating expenses, refinancing debt, or renegotiating loan terms with lenders. Seeking the advice of a financial professional can also help identify strategies to improve the DSCR.

Conclusion

The DSCR Calculator emerges as an indispensable tool in the financial toolkit of lenders and investors, especially within the commercial real estate sector. By providing a straightforward yet powerful way to evaluate a property’s ability to generate enough income to cover its debt obligations, it plays a pivotal role in decision-making processes.

While it offers a quick glimpse into the financial viability of an investment, it’s crucial to integrate its insights with a broader financial analysis. Remember, a higher DSCR ratio signals a stronger, more reliable investment, but it’s just one piece of the complex puzzle of financial health. Therefore, using this calculator wisely, in conjunction with other financial tools and considerations, can pave the way for more informed, strategic investment choices.

Emily Johnson is a seasoned loan expert whose passion lies in empowering individuals to make informed financial decisions. With years of experience in the lending industry, Emily has honed her expertise in various loan products and strategies.